Something strange happened to America’s stock markets over the past three decades. We went from nearly 6,000 publicly traded companies in the mid-1990s to roughly 4,000 today. That’s not a gentle decline: it’s a dramatic reshaping of how American business operates.

For founders, fund managers, and anyone involved in capital raising, this shift changes everything. The public markets that once represented the gold standard exit strategy have become a much smaller club. Understanding why this happened: and what it means for your next deal: isn’t just academic curiosity. It’s essential intelligence for navigating today’s capital landscape.

![]()

The numbers don’t lie

The scale of this transformation is staggering. Public company listings peaked around 1997 at nearly 6,000 firms, then began a steady retreat. By 2020, only about 4,000 companies remained listed on major exchanges. Some analyses put the decline even steeper, tracking a fall from more than 7,000 public firms to fewer than 4,000.

![]()

![]()

The timeline tells its own story. From 1975 to 1997, the number of public companies actually grew by 54 percent. Then came the reversal. The most brutal period hit between 2001 and 2010, when approximately 3,300 companies exited while only 1,800 new ones entered. The following decade saw things stabilize somewhat, with exits and new entries roughly balanced at around 2,100 each.

But here’s what makes this more than just a numbers game: the companies that disappeared weren’t mostly failing businesses. About 95 percent of exits happened through acquisitions, not bankruptcies. This wasn’t creative destruction: it was strategic consolidation.

![]()

The regulatory burden theory

The conventional wisdom points fingers at regulatory costs. Sarbanes-Oxley, Dodd-Frank, and a parade of compliance requirements have made being public expensive and complicated. For smaller companies especially, the cost-benefit equation changed dramatically.

Meanwhile, private capital markets got easier to access. Rule changes allowed private companies to raise significant capital without the public market hassles. Why deal with quarterly earnings calls, activist investors, and SEC filings when you can raise $50 million privately with a fraction of the headache?

This explanation feels intuitive, but it’s probably incomplete. Regulatory costs hit all companies, yet the decline wasn’t uniform across sectors. Something deeper was happening.

![]()

The real culprit: industrial evolution

The more compelling explanation isn’t about regulation: it’s about business itself evolving. Industries that once supported hundreds of mid-sized competitors now reward scale and integration. Technology made some business models obsolete while creating massive advantages for others.

Take banking. The fragmented system of regional and community banks made sense when crossing state lines was legally complicated. As those restrictions fell away, consolidation became inevitable. Bigger banks could invest in better technology, spread compliance costs across larger operations, and offer more comprehensive services.

![]()

![]()

Similar dynamics played out across industries. In technology hardware and semiconductors, research and development costs soared while product lifecycles shortened. Only companies with massive scale could survive. The result? Wave after wave of mergers and acquisitions.

This “industrial organization” theory explains why we have fewer companies but more economic activity. The remaining firms didn’t just get bigger: they got more efficient and profitable.

![]()

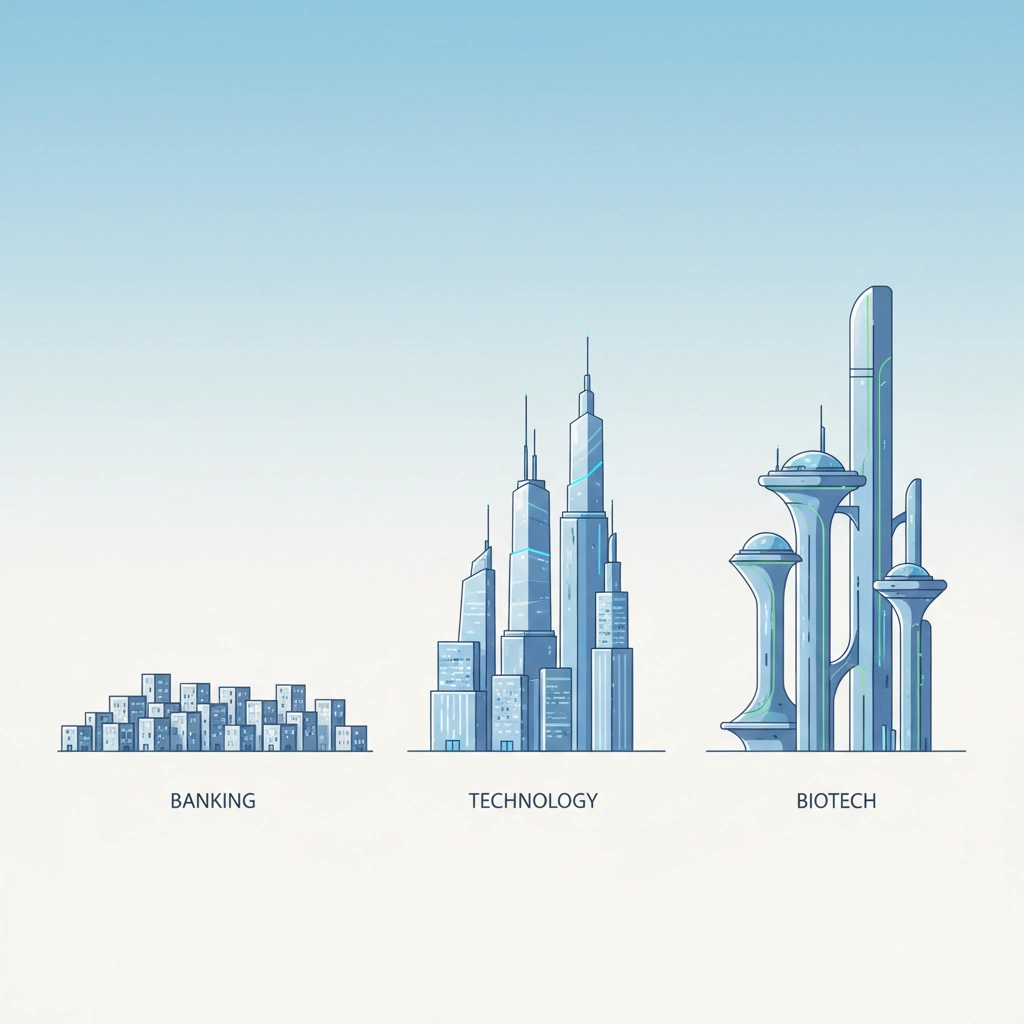

Sector-by-sector breakdown

The decline wasn’t evenly distributed. Banking, traditional industrials, and technology hardware saw the steepest drops. These sectors shared common characteristics: high fixed costs, regulatory complexity, and competitive dynamics that rewarded scale.

But one sector bucked the trend entirely: pharmaceuticals and biotechnology. Between 2011 and 2020, biotech saw more than twice as many new public entrants as exits. This reflects a fundamental shift in how drug discovery works. Instead of massive integrated pharmaceutical companies doing all their own research, the industry now relies heavily on venture-backed biotech startups pursuing focused programs.

The biotech boom illustrates something crucial: the public markets aren’t dying universally. They’re becoming more selective about which types of businesses they reward.

![]()

What this means for founders today

If you’re building a company, the vanishing act of public companies creates both challenges and opportunities. On the challenge side, IPOs have become harder to achieve and maintain. Public investors now expect larger revenues, clearer paths to profitability, and more defensible competitive positions before they’ll support new listings.

![]()

![]()

But the opportunities are equally significant. Private capital markets have exploded to fill the gap. Venture funds, private equity, and alternative lending sources offer more options than ever for companies that might have gone public in earlier decades.

The key is understanding which path makes sense for your specific situation. Companies with strong unit economics and clear market leadership positions might still benefit from public markets. The transparency and permanent capital can support long-term strategic initiatives. But companies in the messy middle: profitable but not dominant, growing but not exponentially: often find private markets more forgiving.

![]()

Implications for fund managers

For private equity and venture capital funds, the public market contraction represents a massive opportunity. With fewer public companies, there are more attractive private acquisition targets. The competition for quality assets has intensified, but so have the potential returns from building and scaling businesses privately.

This shift also changes exit strategies fundamentally. Where IPOs once provided predictable liquidity events, strategic acquisitions by larger companies have become the primary exit mechanism. This puts a premium on understanding which acquirers are actively consolidating in specific sectors.

![]()

The private capital explosion

Private markets didn’t just benefit from public market decline: they actively contributed to it. Private equity assets under management grew from roughly $1 trillion in 2000 to over $7 trillion today. This capital needed somewhere to go, and acquiring public companies became an increasingly attractive option.

The dynamics are self-reinforcing. As more capital flowed into private markets, valuations for private acquisitions increased. This made staying private more attractive for potential IPO candidates, further reducing the flow of new public companies.

Meanwhile, established public companies faced pressure from both directions. Private equity offered premium valuations for going-private transactions, while public market investors demanded ever-higher performance standards.

![]()

Looking ahead: permanent change or cyclical shift?

The big question for decision-makers is whether this transformation represents a permanent structural change or a cyclical shift that might reverse. The evidence suggests permanence. The underlying drivers: technology-enabled scale advantages, regulatory complexity, and abundant private capital: show no signs of reversing.

However, recent developments hint at potential changes. The rise of SPACs, direct listings, and other alternative public market structures suggests innovation in how companies access public capital. Meanwhile, regulatory attention to private market concentration might eventually swing the pendulum back toward policies that encourage public listings.

![]()

Practical implications for capital strategy

For companies and fund managers developing capital strategies, several principles emerge from this analysis:

Size matters more than ever. The public markets increasingly reward scale and market leadership. If your business model doesn’t support becoming a dominant player in a large market, private capital may offer better long-term flexibility.

Timing has changed. The traditional progression from venture capital to IPO to mature public company has been disrupted. Many companies now stay private longer, using multiple rounds of private capital to reach larger scale before considering public markets.

Industry dynamics drive decisions. Sectors experiencing active consolidation offer different opportunities than those supporting multiple viable competitors. Understanding your industry’s trajectory is crucial for choosing the right capital path.

![]()

![]()

The great public market vanishing act isn’t just a statistical curiosity: it’s a fundamental shift in how American business operates. For founders, investors, and advisors, recognizing this new landscape and its implications is essential for making informed capital allocation decisions. The public markets that remain are smaller but more selective, while private capital markets have expanded to fill much of the gap.

Success in this environment requires understanding not just the numbers, but the underlying forces that created them. The companies and funds that thrive will be those that adapt their strategies to this new reality rather than hoping for a return to the past.

This material was provided by artificial intelligence systems and is not intended as investment, tax, or legal advice. Readers should consult qualified professionals for guidance specific to their circumstances.